There was a time when all swans were white. Just like the sky was blue and the grass was green. This was held as a truth until, in the year 1697, a black swan was discovered in Western Australia.

Since then, black swans have become a synonym for the unexpected, the disruptive. Disruptive not only in the sense of paradigm-altering technology phenomena like Google or the iPhone, or business models like Amazon’s or Uber’s. Disruptive also in the sense of geo-politics like the terror attacks of September 11, 2001, the effects of global warming or the COVID19 pandemic. Disruptive also in the political sense such as the UK’s unexpected “Brexit” decision or the rise to power of a complete political outsider to the U.S. presidency.

The 2007 bestselling book “The Black Swan” by Nassim Nicholas Taleb subtitled “The impact of the highly improbable” is said to have prophesized the U.S. banking crash a year later. The premises for a Black Swan event, according to Taleb, are that they are outliers of extreme impact that “human nature” tries to rationalize after the fact by concocting explanations that make them explainable and predictable.

It feels like Black Swans have since conquered the world much like the North American gray squirrel decimated the reddish brown squirrel in large parts of Europe. 2020 in particular has been a year in which it was quite predictable that the unpredictable would happen. The outlier has become the new normal.

While many of these events were negative or even catastrophic in nature, I don’t think we should succumb to a doomsday perspective of life. Out of the chaos, new and good things may emerge if we are open to changing and adopting. A drive to change is not in the human nature, of course, and most will try to cling to present day business models and five year plans. But the Black Swans are here to stay, they are sharing the pond with our beloved white swans. It is safe to say that raw materials and the world’s resources will continue to remain among the White Swans in the world, although not shielded from the effects of economic change and investor behavior. Which is why I decided it was time for a new chapter of this blog series, shifting focus from Metal Megatrends to the White Swan effect precious metals, rare earth elements and technology metals.

It only took me two years, I know… reconciling my new career at BASF with my writing activities was one aspect I kept struggling with. As I experienced in an earlier media exposure, it is ever so easy to see your contents relabeled as the statement of a company or organization you are affiliated with, turning a personal statement into one of that entity. I didn’t want that to happen. In this small world, I also didn’t want to expose people that are dear to me to suspicions of having provided me with insider information even when my actual source is someone else. Appearances alone suffice to pass judgement these days.

So here I am, back and full of ideas for topics, reports and interviews to try and rationalize the irrational before it occurs, instead of after the fact. A bit of an experiment, so let’s see how it goes.

Thanks a lot to my subscribers for hanging in – my new series will start at the beginning of January.

This is what I love most about the precious metals industry: more than 30 years in the business and the learning never stops. Back in 2017, I got myself into a pickle by promising the European Chapter of IPMI a paper on Osmium for their annual conference. At this point, I didn’t even like Osmium which had caused me several headaches back in my Degussa (the original one) days. The market is small, applications are few and to make matters worse, the metal forms a toxic substance when exposed to air, raising the question whether it is as much a precious metal as Pluto was a planet.

This is what I love most about the precious metals industry: more than 30 years in the business and the learning never stops. Back in 2017, I got myself into a pickle by promising the European Chapter of IPMI a paper on Osmium for their annual conference. At this point, I didn’t even like Osmium which had caused me several headaches back in my Degussa (the original one) days. The market is small, applications are few and to make matters worse, the metal forms a toxic substance when exposed to air, raising the question whether it is as much a precious metal as Pluto was a planet.

Please pardon the prolonged absence. As some of you already know, I made a career change earlier this year. Joining BASF takes me full circle as head of their Precious Metals Chemicals business. On top, I am in charge of battery recycling and fuel cell materials which means I was put right into the candy store of Metal Megatrends.

Please pardon the prolonged absence. As some of you already know, I made a career change earlier this year. Joining BASF takes me full circle as head of their Precious Metals Chemicals business. On top, I am in charge of battery recycling and fuel cell materials which means I was put right into the candy store of Metal Megatrends.

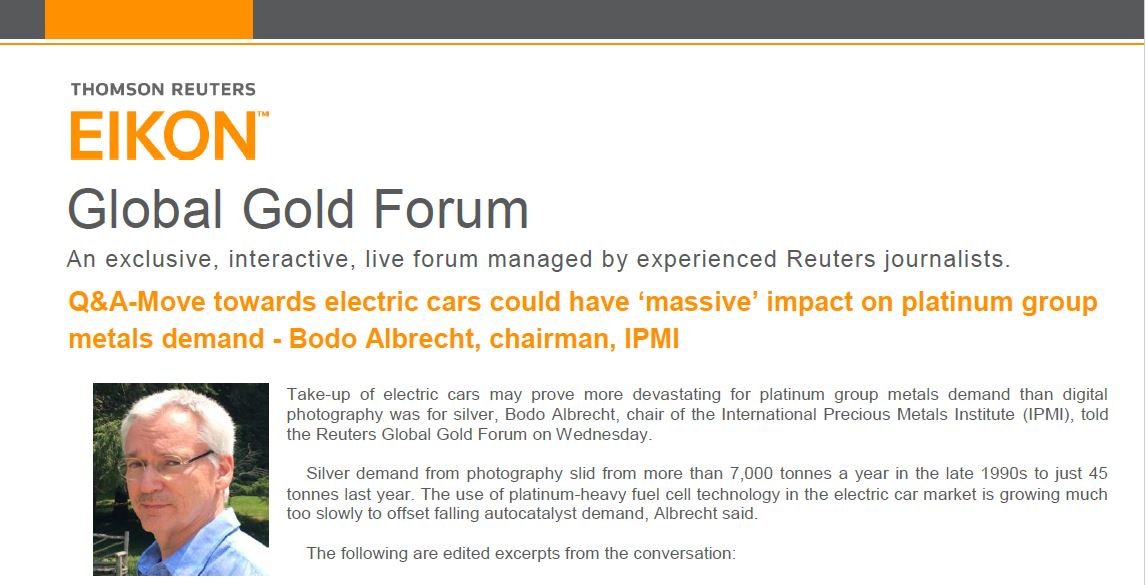

Fuel cell electric vehicles (FCEV) vs. battery electric vehicles (BEV) – the precious metals industry is rightfully concerned about this battle. While FCEVs will utilize platinum in their fuel cells, BEVs need none, and each electric vehicle sold of either kind means that one less standard emission control catalyst has been sold. Reason for Reuters to inquire about the scale of the potential effects.

Fuel cell electric vehicles (FCEV) vs. battery electric vehicles (BEV) – the precious metals industry is rightfully concerned about this battle. While FCEVs will utilize platinum in their fuel cells, BEVs need none, and each electric vehicle sold of either kind means that one less standard emission control catalyst has been sold. Reason for Reuters to inquire about the scale of the potential effects.

One topic of my annual “Metal Megatrends” paper at the recent IPMI conference in Phoenix was sustainable mobility, and its impacts on metal consumption. In fact, if you read the story of how my column for Kitco News started four years ago (see the “Welcome” page of this blog), we have now reached a point where we can answer the question: “What if all cars in the world were electric?”.

One topic of my annual “Metal Megatrends” paper at the recent IPMI conference in Phoenix was sustainable mobility, and its impacts on metal consumption. In fact, if you read the story of how my column for Kitco News started four years ago (see the “Welcome” page of this blog), we have now reached a point where we can answer the question: “What if all cars in the world were electric?”.

The picture shows people waiting at a factory owned store in a shopping mall (Short Hills Mall in New Jersey, USA). The line, which security estimated to be at least 200 people, winds throughout the mall and out the door. The line in the other picture shows people waiting for the new iPhone, also released today in what can only be called a marketing blunder.

The picture shows people waiting at a factory owned store in a shopping mall (Short Hills Mall in New Jersey, USA). The line, which security estimated to be at least 200 people, winds throughout the mall and out the door. The line in the other picture shows people waiting for the new iPhone, also released today in what can only be called a marketing blunder.  It is not the Tesla Model 3 other EV manufacturers have to worry about, it’s the way in which Elon Musk and the Tesla brand excite the masses. The Model 3 presale takes thousands of committed EV buyers off the market for at least 4-5 years (1.5 years of waiting time plus a 3 year lease). Whichever product or marketing strategy other brands may come up with, from hereon the market has been captured by Tesla for a very long time. A VERY smart move.

It is not the Tesla Model 3 other EV manufacturers have to worry about, it’s the way in which Elon Musk and the Tesla brand excite the masses. The Model 3 presale takes thousands of committed EV buyers off the market for at least 4-5 years (1.5 years of waiting time plus a 3 year lease). Whichever product or marketing strategy other brands may come up with, from hereon the market has been captured by Tesla for a very long time. A VERY smart move.

Carlos Ghosn, CEO of both Renault and Nissan, shared some very relevant insights on why electric vehicles are unstoppable, and why he does not see any of the tech companies enter the automotive market as a producer. Ghosn gave a speech at the opening ceremony and press breakfast of this year’s New York International Auto Show (NYIAS). My Kitco report (click

Carlos Ghosn, CEO of both Renault and Nissan, shared some very relevant insights on why electric vehicles are unstoppable, and why he does not see any of the tech companies enter the automotive market as a producer. Ghosn gave a speech at the opening ceremony and press breakfast of this year’s New York International Auto Show (NYIAS). My Kitco report (click

Terms like precious metals, rare earth elements, rare metals, minor metals, specialty metals etc. are used throughout reports leaving many people confused about what they actually mean. The term “Technology Metals” is, admittedly, loosely defined as well. Time for some definitions:

Terms like precious metals, rare earth elements, rare metals, minor metals, specialty metals etc. are used throughout reports leaving many people confused about what they actually mean. The term “Technology Metals” is, admittedly, loosely defined as well. Time for some definitions:

2015 was not a good year for technology metals (precious metals, rare earth elements and strategic metals). From a perspective of industrial use, what is the likely development in demand and price in 2016? Part one of my condensed analysis was just published exclusively on Kitco News.

2015 was not a good year for technology metals (precious metals, rare earth elements and strategic metals). From a perspective of industrial use, what is the likely development in demand and price in 2016? Part one of my condensed analysis was just published exclusively on Kitco News.